The financial world is buzzing as qualcomm stock draws attention after major openai news, signaling a potential paradigm shift in the consumer electronics and semiconductor landscapes. Investors and tech enthusiasts alike are closely monitoring the developments, as rumors suggest that the AI juggernaut OpenAI is pivoting toward custom hardware. By reportedly partnering with industry titans like Qualcomm (QCOM) and MediaTek, OpenAI aims to develop an entirely new category of “AI agent” devices. This revelation comes at a critical juncture for Qualcomm, a company currently navigating significant headwinds in its traditional smartphone handset business.

The OpenAI Catalyst: Redefining Consumer Hardware

For years, the smartphone industry has iterated on a familiar formula: glass rectangles populated by grids of applications. However, the reported collaboration between OpenAI and Qualcomm suggests a radical departure from this norm. The goal is straightforward yet highly ambitious: to build an “AI agent” device that tightly integrates the operating system, hardware architecture, and localized large language models (LLMs). Rather than opening discrete apps to perform tasks, users would interact with a pervasive AI layer that understands context, executes complex multi-step workflows, and anticipates user needs.

“Feels like a good time to seriously rethink how operating systems and user interfaces are designed.”

This sentiment, previously echoed by OpenAI leadership, underscores the foundational shift in how we might interact with technology by the end of the decade. For Qualcomm, this introduces a fascinating new layer to its long-term growth story. The company has long been the dominant force in premium Android processors, but the mobile market has matured. Securing meaningful silicon content—specifically custom Neural Processing Units (NPUs) and integrated AI chipsets—in a genuinely novel device category opens the door to a massive replacement cycle that sits largely outside the traditional smartphone constraints.

The Timeline and Scale of the Opportunity

While the strategic upside is immense, investors must temper their near-term expectations. This project is characterized as “long-dated optionality.” Developing custom silicon tailored for a proprietary AI operating system is a multi-year endeavor. Analysts estimate that product specifications and supplier decisions will not be finalized until late 2026 or early 2027, with mass production targeted for 2028. To understand the scale of what is at stake, consider that the high-end smartphone market currently ships between 300 million and 400 million units annually.

| Phase | Estimated Timeframe | Key Milestones & Impact |

|---|---|---|

| Research & Development | 2024 – Mid 2026 | Initial prototyping, OS integration testing, and core NPU design. No immediate EPS impact. |

| Supplier Finalization | Late 2026 – Q1 2027 | Locking in Qualcomm vs. MediaTek market share. Potential valuation expansion based on design wins. |

| Mass Production & Launch | 2028 | Commercial availability. Potential to trigger a 300M+ unit global hardware replacement cycle. |

Near-Term Hurdles: The Reality of Q2 2026 Earnings

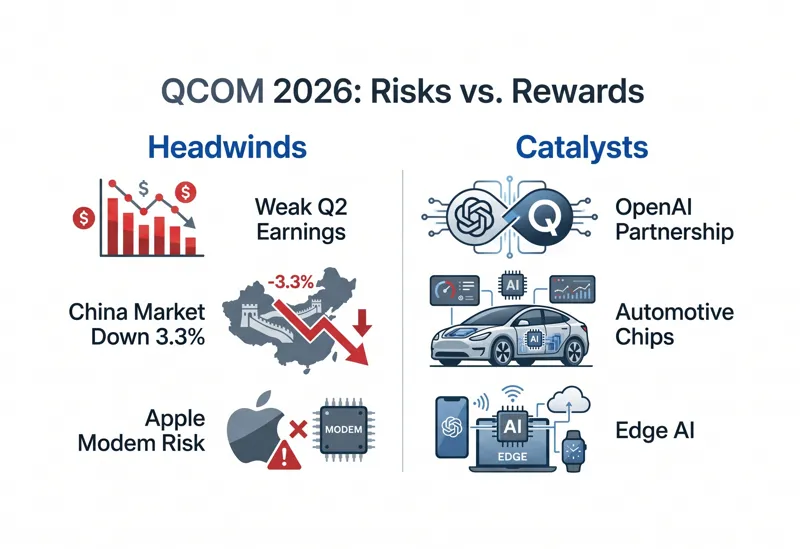

Despite the futuristic allure of the OpenAI project, Qualcomm’s immediate reality is anchored in its core handset business, which is currently experiencing significant turbulence. As Qualcomm approaches its Q2 earnings, the company has guided for revenue in the range of $10.2 billion to $11.0 billion, with adjusted EPS expected between $2.45 and $2.65. For Wall Street, this guidance was notably underwhelming, sparking a sharp sell-off following the Q1 reports.

Management has attributed this softness to sluggish Original Equipment Manufacturer (OEM) demand and conservative inventory behavior driven by higher memory prices. The crucial distinction management attempted to make is that the shortfall is entirely about “build economics”—the cost-benefit analysis OEMs do when purchasing components—rather than a loss of market share to competitors or Apple. For deep dives into their historical earnings data, investors frequently consult Qualcomm’s official investor relations page.

“The key debate for investors in 2026 is whether the current handset softness is a short-cycle inventory pause or a deeper structural decline.”

The macroeconomic backdrop supports a cautious approach. For instance, smartphone shipments in critical markets like China fell by 3.3% year-over-year in early 2026. This indicates that end-user demand is not providing the necessary safety net for component suppliers. If this downturn is merely a cost-driven pause due to elevated memory prices, orders should theoretically recover as component costs normalize in the second half of the year. However, if consumer fatigue has set in, Qualcomm may be entering the next phase of its business cycle from a much weaker baseline.

| Financial Metric | Q2 2026 Guidance | Market Context |

|---|---|---|

| Projected Revenue | $10.2B – $11.0B | Reflects OEM caution and delayed chipset purchases. |

| Adjusted EPS | $2.45 – $2.65 | Pressured by lower volumes and shifting product mix. |

| China Market Growth | Down 3.3% YoY | A major headwind, as China represents a massive premium Android base. |

The Structural Threat: Apple’s In-House Silicon Transition

Even if the broader Android market stabilizes and the OpenAI hardware project materializes, Qualcomm faces a looming structural risk that cannot be ignored: Apple. Apple remains Qualcomm’s highest-profile and arguably most lucrative customer. Estimates for FY2025 indicated that Apple-related revenue accounted for roughly $8.8 billion of Qualcomm’s top line. More alarmingly, an estimated $3 billion of that revenue is directly at risk as Apple aggressively works to replace Qualcomm’s baseband modems with its own proprietary, in-house silicon.

This transition is critical for Qualcomm’s valuation. Apple is a high-volume, high-value customer that significantly bolsters Qualcomm’s margins and helps absorb the massive fixed costs associated with semiconductor research, development, and fabrication. Losing a substantial portion of this revenue inevitably reduces economies of scale, directly impacting profitability. The core valuation question for analysts today is whether this impending loss is already fully priced into QCOM shares. If current consensus estimates still bake in too much Apple-derived revenue for FY2026 and FY2027, the stock could face further downward earnings revisions, regardless of how the broader handset market performs.

Evaluating the Road Ahead: Catalysts and Downside Risks

For investors analyzing Qualcomm’s current position, the narrative is a complex blend of short-term pain and tantalizing long-term potential. The company’s future hinges on several pivotal factors across different time horizons. The transition from being a pure-play smartphone chip provider to a diversified computing company powering automotive, edge AI, and novel AI-agent devices is underway, but the road is fraught with execution risks.

“If Qualcomm secures a leading role in the AI-native device category, it creates massive upside optionality outside the traditional smartphone market, cementing its relevance for the next decade.”

To summarize the complex investment thesis surrounding QCOM in 2026, we must weigh the potential upside drivers against the structural pressures bearing down on the stock.

| Potential Upside Catalysts | Downside Pressures & Risks |

|---|---|

| Successful, exclusive partnership with OpenAI for the new AI agent hardware. | Another weak quarterly guide confirming a structural handset slowdown. |

| OEM orders normalize rapidly in H2 2026 as memory component costs ease. | Apple accelerates its modem insourcing, stripping away high-margin revenue faster than expected. |

| Android demand stabilizes in China, supporting a strong recovery in premium Snapdragon builds. | Deepening weakness in the Chinese smartphone market, pressuring device mix and overall margins. |

| Automotive and edge AI segments scale up, successfully diversifying earnings. | The rumored AI device initiatives face engineering delays or fail to materialize entirely. |

Conclusion: Balancing Short-Term Reality with Long-Term Vision

Qualcomm stands at a fascinating crossroads. The core handset business is undeniably under pressure from macroeconomic weakness, high component costs squeezing OEMs, and the looming threat of Apple’s modem insourcing. The upcoming Q2 earnings report will be a crucial litmus test to determine if the current weakness is a mere inventory blip or a more entrenched structural issue.

However, the revelation of the OpenAI hardware project injects a powerful dose of optimism into the long-term narrative. If Qualcomm can leverage its unmatched expertise in mobile processing, power efficiency, and integrated AI to become the silicon backbone of the first true “AI agent” device, the company could trigger a massive new growth cycle. For now, investors must balance the tangible, near-term execution risks in the smartphone market against the immense, albeit distant, potential of an AI-native hardware revolution.

Frequently Asked Questions (FAQs)

Why is Qualcomm stock drawing attention regarding OpenAI?

Reports indicate that OpenAI is exploring the development of a custom “AI agent” hardware device and is considering a partnership with Qualcomm (and potentially MediaTek) to supply the specialized processors required to run local AI models efficiently.

What is an “AI agent” device?

Unlike traditional smartphones that rely on a grid of disparate apps, an AI agent device integrates an AI model directly into the operating system and hardware. It is designed to act as a cohesive digital assistant capable of anticipating needs and executing multi-step tasks across the system without manual app navigation.

Will the OpenAI project impact Qualcomm’s earnings this year?

No. The OpenAI hardware project is considered long-dated optionality. Product specifications are not expected until late 2026 or 2027, with mass production targeted for 2028. It will not impact Qualcomm’s immediate FY26 or FY27 financials.

Why is Qualcomm’s Q2 2026 guidance considered weak?

Qualcomm guided for revenue between $10.2 billion and $11.0 billion, which disappointed the market. Management cited softer OEM demand and paused orders caused by high memory prices, which squeezed handset build economics.

How does the Apple modem transition affect Qualcomm?

Apple is actively developing its own in-house modems to replace Qualcomm’s components. With an estimated $8.8 billion in total Apple-related revenue (and roughly $3 billion immediately at risk), this transition poses a significant structural threat to Qualcomm’s high-margin business.

Is the current smartphone market downturn a short-term or long-term issue?

This is the primary debate among analysts. Optimists view it as a short-cycle inventory pause driven by component costs that will resolve in late 2026. Pessimists point to shrinking shipments in major markets like China (down 3.3% YoY in Q1) as evidence of a deeper, structural demand problem.

What are Qualcomm’s growth avenues outside of standard smartphones?

Beyond the potential OpenAI partnership, Qualcomm is heavily investing in diversifying its revenue streams by expanding into the automotive sector (digital chassis and autonomous driving chips), edge computing, IoT, and advanced PC processors via its Snapdragon X Elite architecture.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The stock market is volatile, and investors should conduct their own thorough research or consult with a licensed financial advisor before making any investment decisions.